For the past two years, we have noted the sharp uptick in delinquencies in installment contracts receivables (ICRs) in 8990 Holdings Inc. (otherwise known by its ticker: HOUSE).

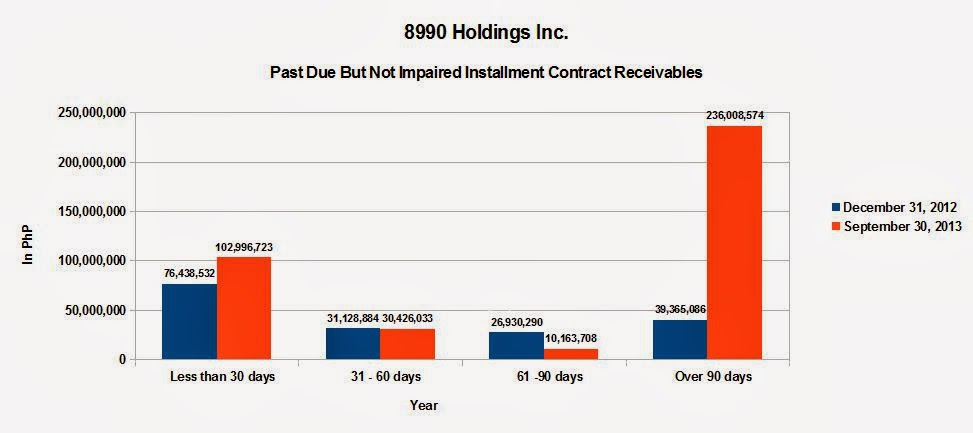

In 2014, in a post entitled "Has the Philippine Real Estate Bubble Already Burst?", we noted a very sharp uptick in HOUSE's ICRs that were over 90 days past due. The marked change was very evident during the period from December 31, 2012 to September 30, 2013.

Impairments of these past due receivables were minimal, climbing from an absolute zero in 2012 to just Php 7.2 million in 2013 or a negligible 0.07% of 8990's total ICR portfolio.

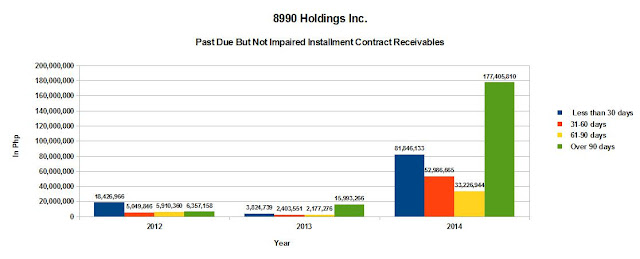

Shortly after that post was published, those past due ICRs mysteriously disappeared in the company's audited 2013 Annual Report (See 8990 Holdings, Inc.: The Case of the Disappearing Past Due Installment Contract Receivables). ICRs that were over 90 days past due dropped from a reported Php 236.0 million as of the September 30, 2013 (Unaudited Interim Report) to just Php 16.0 million as of December 31, 2013 (Audited Annual Report).

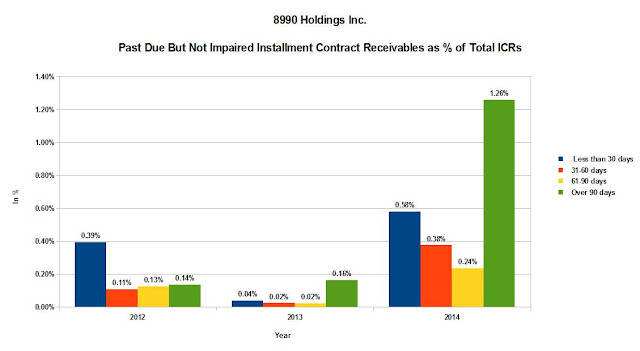

Those disappearing past due ICRs miraculously reappeared in the 2014 Annual Report, when HOUSE report that Php 177.4 million or 1.26% of its ICRs were over 90 days past due (See: "The Philippine Real Estate Bubble Has Already Burst for HOUSE (8990 Holdings, Inc.)".

These are the money shots:

Impairments showed "hockey stick"-like exponential growth, jumping from just Php 7.2 million or 0.07% of Total ICRs in 2013 to Php 1.4 billion or a staggering 9.84% of Total ICRs as of year-end 2014.

Today, the pig is out of the python. The "pig" of Impaired ICRs has almost doubled to more than 18.14% of the total ICR portfolio (the python).

But ICRs that are over 90 days past due has dropped considerably from Php 177.4 million or 1.26% of total ICRs in 2014 to just Php 100.6 million in 2015 or 0.53% of total ICRs in 2015. This could mean that the pipeline of incoming impairments (meaning 90-day past due ICRs) may have stalled or even dropped.

This could mean that 8990 now has a better handle on screening its customers for credit worthiness. It could also mean that the Philippine real estate market has stabilized. Volumes for the overall market have remained stable and home prices have continued their upward trend.

Socialized housing, the market space where 8990 predominantly operates has also done well in 2015. So this could be a factor as well.

8990 remains heavily exposed to areas outside Metro Manila. Over 50% of its ICRs are in Davao and Cebu. Exposure to the Metro Manila market is minimal, only 2.11% of ICRs are originated in Metro Manila.

And that could be a good thing.

Source: 8990 Annual Reports, 2012 to 2015; HLURB, edge.pse.com.ph

{kind=link}

{kind=link}