The same holds true for the real estate market.

US Real Estate Market

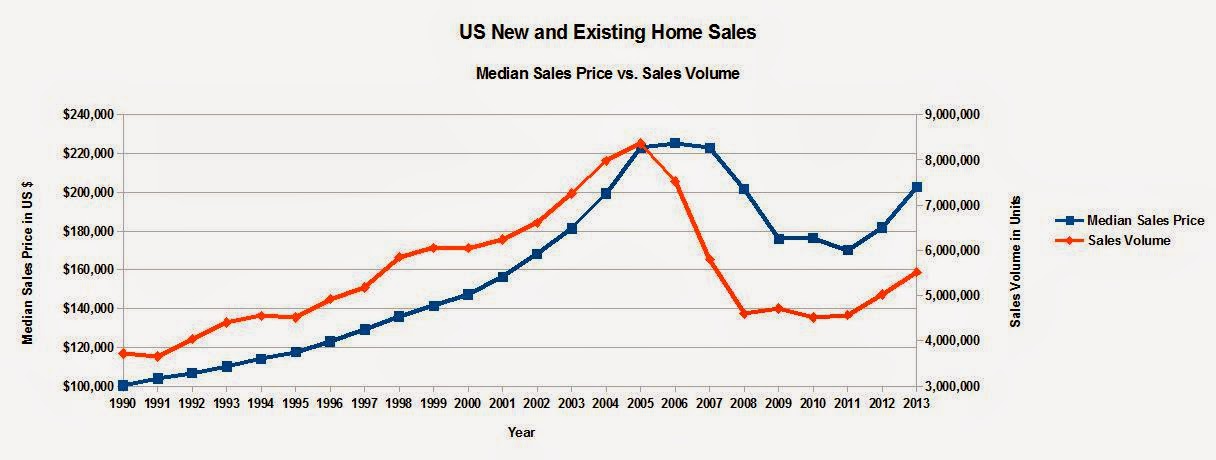

In the US, sales volumes peaked for US Total Home Sales (New and Existing Home Sales) at 8,4 million homes in 2005, a year before the US Median Sales Price peaked at US$ 225K in 2006. By 2007, the US Median Sales Price slipped by only 1% to US$ 223K while sales volumes had already dropped an astonishing 30.58% from the peak sales volume in 2005, to 5.8 million in 2007.

From then on, the US Median Sales Prices continued to decline year after year, bottoming out at $170K in 2011, or some 25% below the peak price level. By then sales volumes had already bottomed out a year earlier in 2010 to 4.5 million homes, or some 46% below peak volumes.

Sources: Realtor.org, St. Louis Fed

Median Sales Price is a weighted average of the median sales prices of New Home Sales and Existing Home Sales

The same dynamic played out in both segments of the US Residential Real Estate Market: New Home Sales and Existing Home Sales.

Here is the chart for New Home Sales:

And here is the chart for Existing Home Sales, the much larger market segment.

Philippine Real Estate Market

Might the same dynamic be playing out in the Philippine residential real estate market? One problem bedevilling such an analysis is the dearth of data.

To my knowledge, the Philippines does not have adequate market data. For instance, there seem to be no published figures for sales volumes for residential homes. The best approximation of such data is HLURB's statistics for licenses to sell residential homes. This statistic represents only new homes and only represents licenses to sell for each residential unit and not the actual sales volumes.

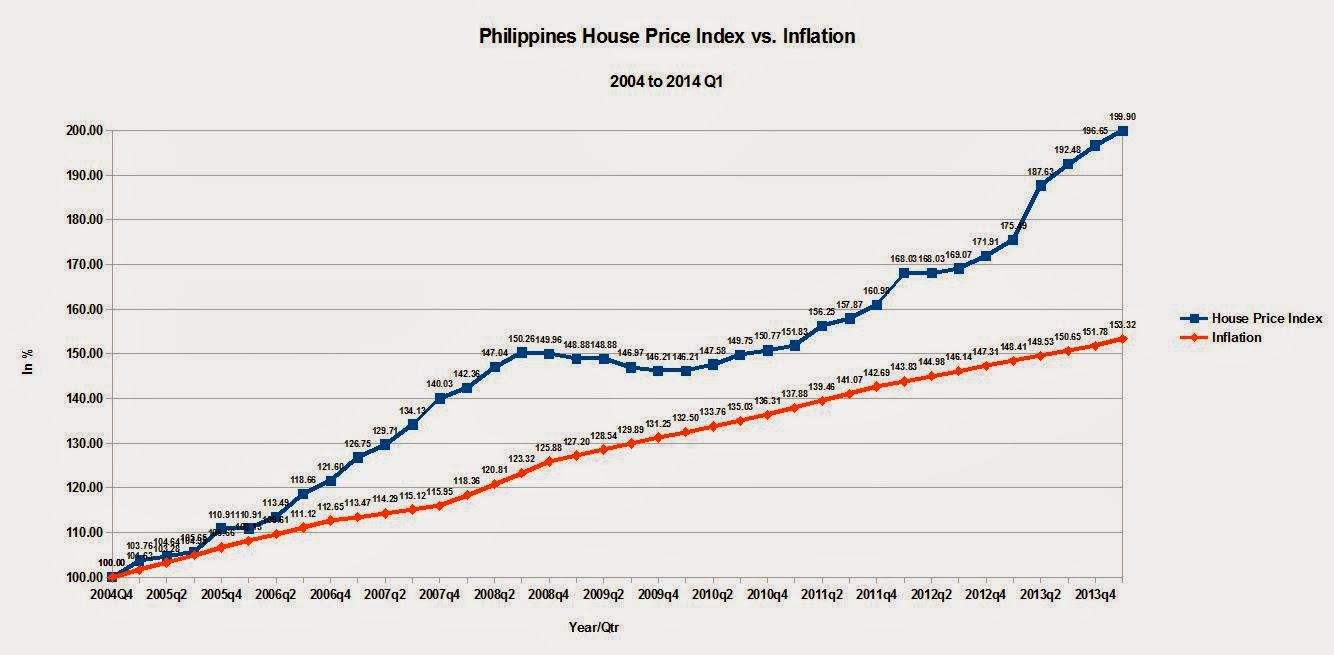

Another issue is that there seems to be no price data on residential sales. The best data is assembled here, which in turn, is assembled from the Philippine Office of Colliers International, a global real estate agency. These prices, in turn, are based on the average prices of a prime 3 bedroom condominium unit in the heart of the Makati Central Business District. This is like basing nationwide US housing prices on the price of a prime 3 bedroom coop unit in Manhattan in New York, one of the priciest real estate markets in the US. The data available in the Philippines is not representative of the true state of the entire national residential real estate market. At best, it is an approximation of the Philippine Real Estate Market. The BSP has stepped into the picture to overcome this deficiency by developing their own real estate index, which would be more comprehensive in scope. Here is a possible candidate for such an index.

But based on the data available, we arrived at this chart:

Based on this data, volumes (as indicated by Residential HLURB licenses to sell) may have already peaked in 2012, while prices have continued their upward climb to date. Volume seems to have peaked at 264,237 units in 2012 and dropped 15% to 225,051 units in 2013. In the first quarter of 2014, volumes declined further on an annualized basis, to just 189,668 units or 28% below peak volumes.

Prices though, have continued to climb since 2012, another 14% in 2013 and another 2% in the first quarter of 2014, representing a 16% increase over 2012 prices.

Is the same dynamic that played out in the US Residential Real Estate Market playing out in the Philippines? It looks like it, but it may still be too early to tell.